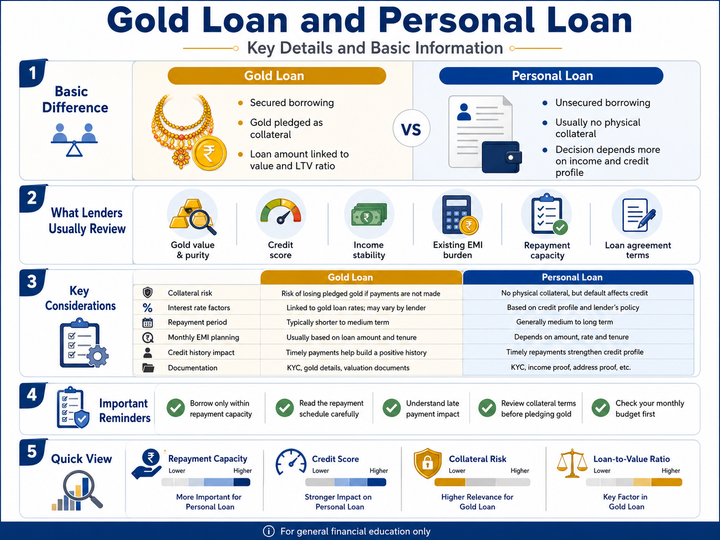

Gold Loan and Personal Loan Guide: Key Details and Basic Information

Gold loans and personal loans are two common forms of borrowing used by individuals in India. Both can help people manage planned or unexpected financial needs, but they work in different ways.